Are you a digital entrepreneur within the European region? Even if you’re not, do you charge EU VAT for digital taxes to your customers in the European Union? At what rate? — Was it even right? Was your client an end-customer, distributor, or retailer? How do you store your invoices?

If you’re reading this and are worried that you have no idea how to answer any of these questions, or probably have an idea but you’re not sure whether it’s the right answer, this one is for you. Naturally, businessmen keep tabs on everything around them for them to be successful. They also have to comply with government rules and regulations for business success.

This applies to VAT rules as well. No matter the size of the online business, or the type of digital goods you are selling, you have to be exceptionally good at observing EU VAT for digital tax rules. Whether you are located in the EU or not, that does not matter. Why so? — Because any time you transact with a customer based in European Union, you have to file and pay tax to the government. What if you don’t? — Simple: If you forget to charge EU VAT for digital tax during the sale, you’ll have to pay yourself.

That said, as long as your customer lives in any of the 28 member countries of the European Union, you’ve got to charge VAT, collect it, then pay it later to the government as you file your EU VAT for digital taxes.

Unfortunately, the area of taxes can be quite confusing for many, and if your constantly disoriented because you just can’t seem to understand the VAT process, you’ll be happy to know that you’re not alone. Even better, we have devised a comprehensive guide to staying compliant with EU VAT for all digital businesses.

Back to the table of contents ⇑

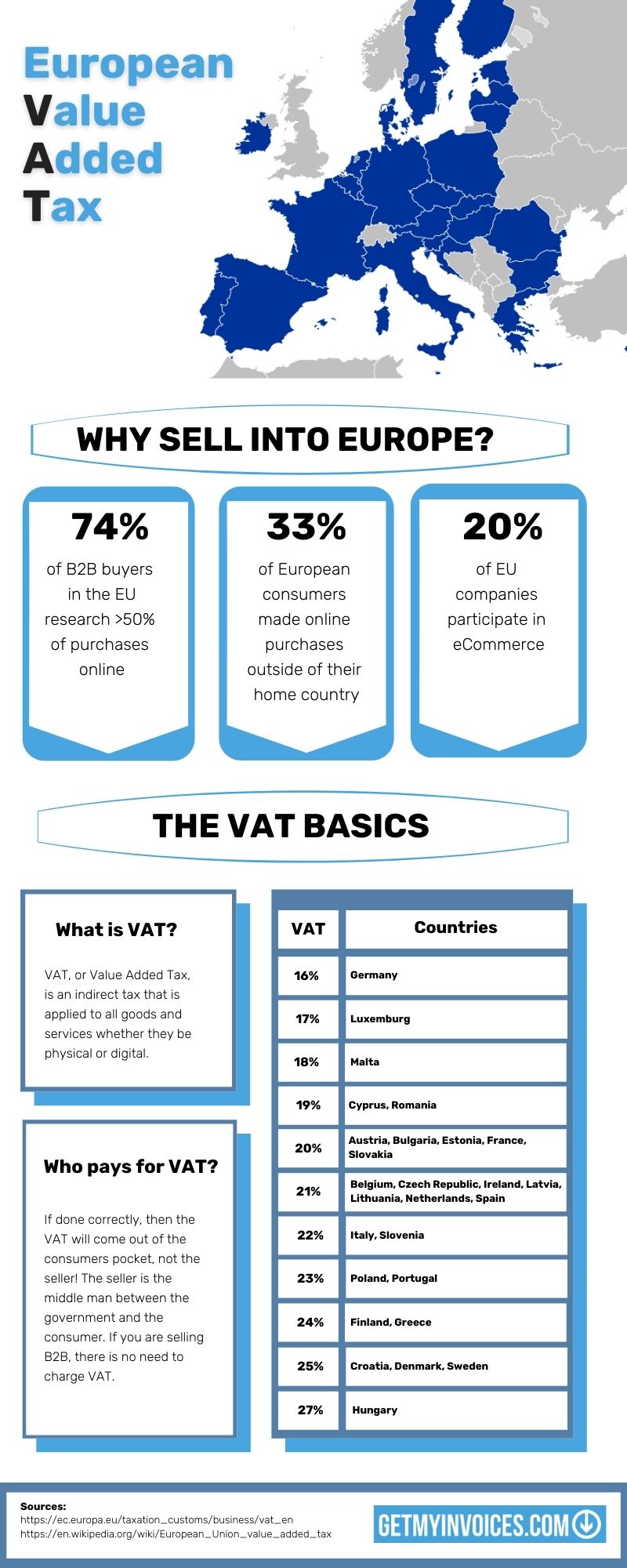

VAT means value-added tax, which means a consumption tax on a service or good. In simple terms, it is a tax that is added to a commodity, usually paid by the consumer, not by a business. As such, every sale made in the EU has a certain percentage of the total cost to be paid to the government.

This percentage ranges anywhere from 16% to 27% depending on the specific country the consumer is located. As a business owner, you, therefore, have to be familiar with all the national rates for each country so that you can add EU VAT for digital tax to your customers in the EU. Specifics on the same will be discussed later in this guide.

Back to the table of contents ⇑

A digital good refers to a product that is used, stored, and delivered in an electronic format. Such goods include downloadable applications and files, products received on email, gotten from the internet, or accessed through a website. Unlike physical goods, digital goods are intangible. Their tax rules, therefore, differ from those governing physical products. You could also hear digital goods referred to as “digital services,” “e-goods,” “e-services,” or “e-commodities”. All these names refer to digital goods.

Sure, the definitions sound a bit ambiguous. After all, how can it be anything stored, delivered, or used in electronic format? — It’s simply too vague. Well, this ambiguity is rightfully placed here.

As the world evolves, technological advancements are improving in the blink of an eye, literally. No other industry is progressing as fast as technology is. As such, we cannot use a narrow, specific, term to define digital goods only to have an unforeseen concept come and knock down our short-sighted definition. So yes, digital goods are broadly categorized, and all fall under one tax regulation category.

Here is the criterion that the European Commission uses to certify that something is indeed a digital good:

The above may seem loosely tied but they provide a specific yet wide window for the enigma that is technology. Even with incoming innovation, where we’ll see digital goods that we only thought existed in Sci-Fi movies, the above criterion is specific but still broad enough to make sure that all types of digital goods are included in the future.

Here are some popular digital goods on the globe today:

Back to the table of contents ⇑

Just like physical commodities, there are times when you do not need to charge VAT. Don’t get us wrong, you need to consider VAT with every sale, but there are times that you do not need to collect it from your customer. It is therefore imperative that every entrepreneur knows when to charge VAT. As such it comes down to 2 major factors:

As a rule of thumb, as long as you’re a European business, you have to charge VAT in your home country. That said, every sale of digital goods has to include the VAT, which should be collected from the consumer. When selling elsewhere in the EU, the transaction can either fall into category B2B or B2C below:

In this case, you normally include VAT and collect it from your customers. As previously indicated, the rate of VAT is not universal, and even in the same country, it can differ depending on how much money you’re making. As long as the business transacts less than €10,000 in cross-border sales of digital goods per annum, throughout the EU, then one can use the VAT rate of the home country on all the cross-border sales. Beyond this threshold, however, the entrepreneur must charge the VAT rate of their customer’s country.

In this case, you do not have to charge VAT. The buyer pays VAT to their government in a reverse-charge method. This way, you do not have to file separate tax returns for every country where you sell. As long as consumers provide you with their VAT numbers during transactions they can file the VAT taxes later. You should verify the clients’ numbers using the VIES service. More on this will be discussed later.

When it comes to countries outside the European Union, it’s pretty much straightforward. Just reverse-charge VAT in B2B situations and charge VAT based on the customer’s country in B2C situations.

Back to the table of contents ⇑

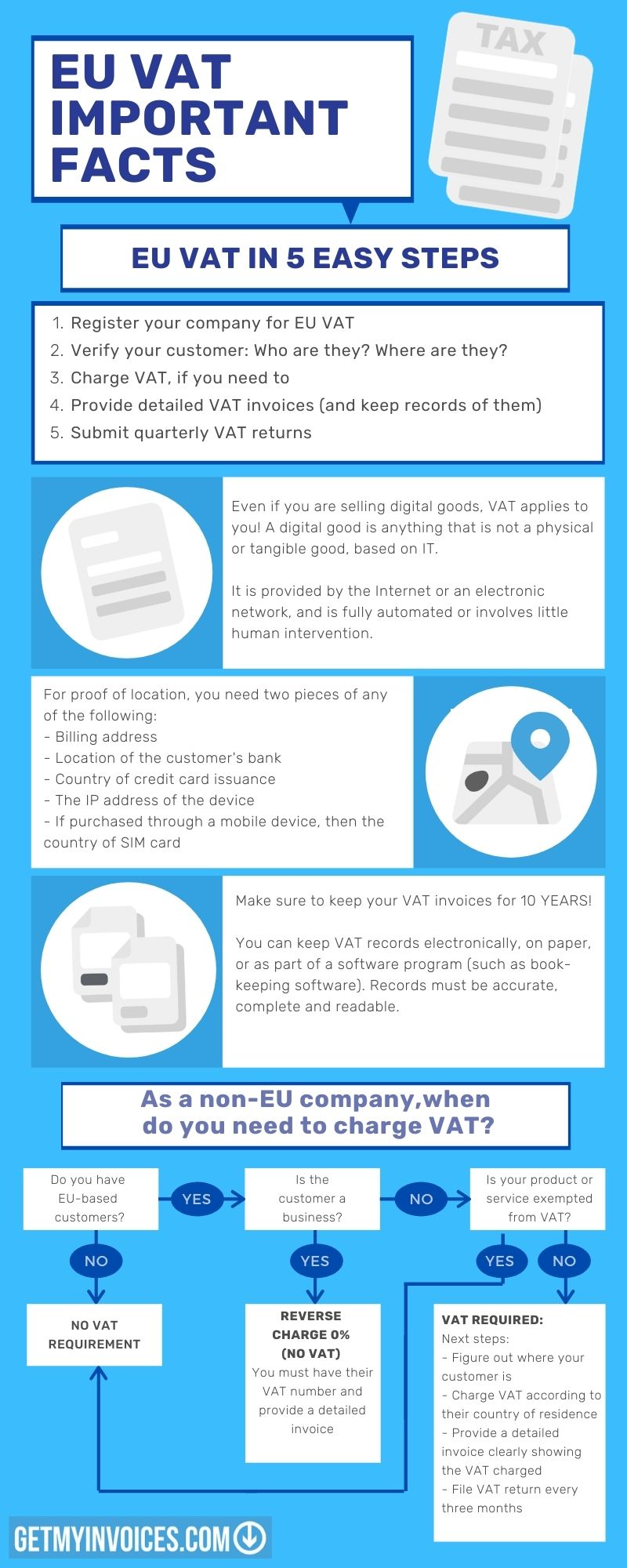

As mindboggling as it sounds, this entire EU VAT digital tax mumble-jumble can be summarized in 5 steps from start to end. Here are the steps to take as an entrepreneur:

Back to the table of contents ⇑

As expected, you first have to register your business for European Union VAT for you to legally conduct any business within the EU. This could be a one or two-step process depending on the county your register from.

Register your business with a tax authority in the EU

If your company is located within the EU, it’s as simple as registering for VAT in your country. If your company is located outside the EU, choose one of the 28 counties to host your tax registration. As such, first sign up with the country’s Mini One-Stop Shop (MOSS), a progressive 21st-century scheme that we’ll explore in detail later on. Confused a bit about the EU country to choose from? Well, don’t fret! Here are some tips:

This way, you will understand all guidelines, processes, and tax documentation without needing a translator. If you’re a native English speaker, you could e.g. take Ireland but there are also other countries like Spain which use English in their tax processes as well.

If you’re in the digital world, you know how frustrating it can be to be slowed down by sluggish and unresponsive websites. Though every EU member of state has to offer an online portal for EU VAT MOSS according to law, some are better than others. We’ll also provide links to each national MOSS page, so you can decide which ones best work for you.

Note that a VAT number differs from a local tax number. The first one allows international sales to other EU countries while the local tax number only permits local transactions. After registering your business, some countries automatically issue you with a VAT number. For others, you will receive a local ta number after which you can apply for a VAT number as a second step.

Back to the table of contents ⇑

All eyes on this part of the article, please! This is one of the most vital steps in staying EU VAT for digital tax compliant during and after the sale. It will not only explain everything you need to know about charging VAT to your clients, but it will also direct you on how much VAT to charge, whether or not you need to charge VAT, and all other information that you need for your tax records.

As soon as you procure a new customer in the EU answer these 2 questions:

This is the first step to knowing whether you need to charge EU VAT for digital tax or not. Assess whether you are selling to another business or end customer. This can be eased by always asking for your customers’ VAT registration numbers. Every business must have a VAT number. If they don’t have one, categorize the transaction as a B2C.

On the other hand, if a customer is a business (B2B), use the VAT registration number to confirm whether the business is valid. Why do you need to double-check this? Because some fraudulent customers will give false VAT registration numbers just to evade EU VAT for digital tax. Use a validation tool from the European commission to countercheck all your VAT registration numbers.

As we have reiterated time and again, VAT rates are not the same for all countries in the EU. You do not want any additional surprise costs during the tax season. As such, make sure you confirm your customer’s location to determine how much VAT you should charge.

Various documents could help you with this, pick any 2 on this list:

Note that if you’re below the €100,000 cross-border sales threshold, you can collect one piece of evidence to verify your customers’ location. To make sure that it is legit, however, you will have to get it from a third party, say the bank, or devices’ IP address, and not directly from your consumer.

What’s more, is that you need to keep this location as evidence for a minimum of 10 years. Such documents keep a record of your tax compliance to ensure that you’re never caught off-guard. That said, keep your digital files either directly in your accounting/tax software or use cloud-based storage.

Back to the table of contents ⇑

Do I need to charge VAT? Here is a quick recap of the guidelines we outlined earlier:

Back to the table of contents ⇑

Bet you already feel that the tax process is exhausting, right? Keep going because it is these taxes that keep the world civilized, productive, and sane. Can you imagine if people had to contribute to infrastructure? I’m sure that all we’d have as a globe are a few electricity poles, highways, and buildings. Taxes keep the people taken care of by their government.

Anyway, enough of the philanthropy. Tedious record keeping is part and parcel of tax keeping, so you better accept it soon enough. Here is the EU VAT for digital tax invoice: It is a supercharged invoice that accompanies every digital sale to indicate the details of all business transactions. It is vital in staying VAT compliant and helps stay organized when filing your tax returns. It also has to be issued when no VAT is charged.

Keep all invoices for at least 5 years in case you need to prove yourself later. In case any EU institution asks for the invoice, you should have all files ready by storing them digitally. This can be done easily and conveniently with our invoice management solution GetMyInvoices. Read how to archive your outgoing invoices quickly and clearly and transfer them automatically to accounting software, billing applications or other solutions.

Back to the table of contents ⇑

The MOSS system, or Mini One-Stop-Shop scheme, makes the last step pretty straightforward. Simply post your returns on this platform, with the MOSS in the country where you’re registered. The MOSS system automatically calculates how much VAT you are required to pay after you fill in the countries that you made sales in.

From here, all you will need to do is pay the VAT in full amount, after which the system disintegrates the VAT and pays them to each government in the EU for you. Even if you’ve sold to 50 customers scattered all over the 28 countries, you’ll not need to stress! How amazing!

Additionally, if you’re an EU-based company making below €10,000 per year in either of the 28 countries, simply file your VAT returns with your home country. You do not need the MOSS system at all. That said, you might not be familiar with when you are needed to file your EU VAT for digital tax returns. It needs to be done at the end of each quarter, within 20 days.

Here are the exact dates and deadlines:

Back to the table of contents ⇑

EU VAT Digital tax rates are not universal. They vary from country to country, ranging from 16% to 27%. This means that you’ll sell your eBooks and videos at different prices for customers in France and Spain, or any other place in the EU. This should not worry you since your competitors are also subjected to similar laws of EU VAT for digital taxes.

Browse the current EU VAT for digital tax rates in all EU countries using the rates list.

Back to the table of contents ⇑

Why don’t you need to charge VAT to EU businesses? Here’s how the reverse-charge mechanism works:

Ideally, in a typical B2B process, a customer would pay VAT to you, you would pay it to the authorities who would then reimburse the amount to the customer after he or she reclaims the amount as a tax break. This method, therefore, leaves the responsibility of paying and filing VAT to the buyer, thereby cutting you out as a middleman. In essence, it is quite logical to cut down this back and forth. You, therefore, don’t need to register for taxes in every EU country when you have a business buyer.

Back to the table of contents ⇑

It was debuted in 2015 to ease the process of filing returns for digital transactions. It makes the process easier since there is no need to apply for VAT registration in each country that a business has a customer. If you are a non-EU-based business, based in the EU country of your choice, or your home country within the EU, look up the process used in registration after registering for a MOSS with the local tax authority.

Following this, the taxes work as annotated below:

There you are! For the complexity of the world of digital taxes, MOSS is a fresh breath of air, to say the least. You can access a list of the MOSS websites for most of the European members here.

Back to the table of contents ⇑

Well … We must admit that it would be disheartening to have to take a longer way out, but for your OWN reasons, you are allowed to!

First, you should register for EU VAT for digital tax in each country where you have a customer. What?! Yes please, it is literally the definition of a hassle!

Second, you should keep all necessary records according to local policies. You should then file returns individually, following each country’s deadline, and file separate tax returns based on each country’s deadlines.

Remember that MOSS only works for businesses that sell over €10,000 per year. This translates to a multi-national customer base. Can you imagine the work that is involved! Talk about coming up with a whole department to deal with VAT! Nevertheless, here are the pros and cons of each system to help you settle for the best:

Back to the table of contents ⇑

I am an entrepreneur dealing with digital goods. Is there any way I can be exempted from EU VAT for digital tax?

Currently, all businesses must file and pay their VAT to EU countries. European businesses that stay below €10,000 in cross-border EU of digital goods per year are the only ones exempted from EU VAT digital taxes. Though they are exempted from the MOSS scheme, they must still collect and file their taxes after selling digital goods and services.

I sell physical goods online. Do I have to pay EU VAT for digital tax?

This guide only applies to digital goods. Physical goods have other VAT rules.

My business is not based in the EU. Do I still have to pay tax?

Yes. VAT can be paid as per the transactions where your buyer does not have a valid VAT number or through the B2C guidelines.

If I decide not to comply with the VAT rules, can I still operate my business?

If you’d like to stay on the right side of the law, you must register for VAT and comply with all regulations. Failure to do this means fines for non-compliance or paying years of back taxes which can be detrimental to your firm.

If I’m selling my products and services through a marketplace, do I have to comply with EU VAT for digital tax rules?

Renowned digital goods’ marketplaces like Bandcamp, Envato, and Amazon Kindle Direct Publishing normally take care of VAT for their clients. However, not all marketplaces do this which is why you need to countercheck the policies that govern your marketplace to avoid landing yourself in trouble.

See the benefits of automated invoice management:

Better overview. Less accounting work. More time for your ideas.

The tax number is needed for many applications and procedures in Germany. However, the tax...

02.02.2021

Tracking and assessing the performance quality of the Accounts Payable (AP) systems in a business...

08.10.2021

Consistent invoicing is a crucial part of every business, and proper invoice management brings healthy...

03.09.2021